11 Years of Pradhan Mantri MUDRA Yojana: Transforming ‘Funding the Unfunded’ into India’s Grassroots Entrepreneurship Revolution

Exactly 11 years ago on this day, Prime Minister Narendra Modi launched the Pradhan Mantri MUDRA Yojana (PMMY) with a bold vision — “Funding the Unfunded”. What began as a scheme to provide collateral-free credit to micro and small entrepreneurs has today emerged as one of India’s most impactful financial inclusion initiatives. As the scheme completes 11 years, it has disbursed over 58 crore loans amounting to more than ₹40 lakh crore, empowering millions of small business owners, especially women and first-time entrepreneurs, across cities, towns, and villages.

The scheme has not only bridged the credit gap for non-corporate, non-farm micro enterprises but has also fostered a culture of self-reliance, turning job-seekers into job-creators and strengthening the foundation of India’s economy at the grassroots level.

From Limited Access to Last-Mile Credit Delivery

For decades, millions of small entrepreneurs — running neighbourhood kirana stores, repair workshops, tailoring units, or allied agricultural activities — struggled to access formal bank credit. Lacking collateral and formal documentation, they often depended on high-interest informal lenders, which stifled growth and increased vulnerability.

The launch of PMMY on April 8, 2015, changed this landscape. Under the scheme, collateral-free loans up to ₹20 lakh are now available for income-generating activities in manufacturing, trading, services, and allied agriculture. The Micro Units Development and Refinance Agency Ltd. (MUDRA) acts as a refinance institution, supporting a wide network of Member Lending Institutions (MLIs) including Scheduled Commercial Banks, Regional Rural Banks, Small Finance Banks, NBFCs, and Micro Finance Institutions. This structured ecosystem ensures credit reaches even the most remote areas.

As of early 2026, the cumulative achievement stands impressive: over 58 crore loan accounts with disbursements exceeding ₹40 lakh crore. Notably, more than 12 crore accounts belong to new entrepreneurs, bringing them into the formal banking system for the first time.

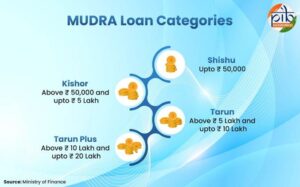

Four Categories to Support Every Stage of Business Growth

PMMY offers tailored loan products based on the enterprise’s growth stage:

- Shishu: Loans up to ₹50,000 – Ideal for beginners and very small businesses with minimal or no credit history.

- Kishor: Loans above ₹50,000 and up to ₹5 lakh – For enterprises needing working capital, stabilisation, or modest expansion.

- Tarun: Loans above ₹5 lakh and up to ₹10 lakh – Targeted at growing businesses looking to scale operations, buy equipment, or increase production.

- Tarun Plus (introduced in 2024 following the Union Budget announcement): Loans above ₹10 lakh and up to ₹20 lakh – Available to successful Tarun borrowers who have repaid previous loans, enabling further expansion.

This graduated structure allows micro-enterprises to start small and gradually scale up with institutional support.

Driving Inclusive Growth: Women and Marginalised Sections Lead the Way

One of the most remarkable aspects of PMMY has been its focus on inclusion. In recent years, women borrowers account for nearly 60-70% of total loan accounts, with significant shares in disbursement amounts as well. This has empowered countless women to achieve financial independence and contribute to household and community economies.

In FY 2024-25, women constituted about 59.81% of loan accounts. New entrepreneurs made up around 21% of accounts, reflecting the scheme’s success in encouraging fresh ventures. Additionally, borrowers from SC, ST, and OBC categories together represent a substantial 45.52% of loan accounts.

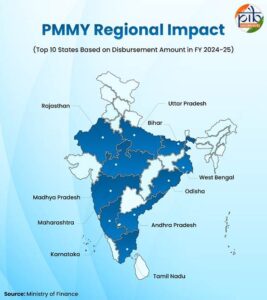

State-wise, Uttar Pradesh has consistently led with the highest disbursements (around ₹58,111 crore in one recent reference year), followed by Bihar and Maharashtra. These figures highlight how PMMY is fuelling economic activity in both populous and emerging regions.

The scheme has also integrated well with digital initiatives. The JanSamarth portal provides a unified platform for multiple credit-linked government schemes, simplifying applications and improving transparency. The Credit Guarantee Fund for Micro Units (CGFMU) further reduces risk for lenders, encouraging more collateral-free lending.

Real Stories of Transformation: Small Loans, Big Dreams

The true impact of PMMY lies in the lives it has changed.

Poonam Kumari, a farmer’s daughter-in-law from Bihar, took an ₹8 lakh MUDRA loan in 2024 to start a seed trading business. With minimal paperwork, she built a venture that now earns her ₹60,000 monthly, bringing financial stability and respect within her family.

In Baramulla, Kashmir, Mudassir Naqshbandi transformed from a job-seeker to a job-creator. His MUDRA-supported bakery, Bake My Cake, now employs 42 people from remote areas. Nine out of ten transactions at his shop happen via UPI, symbolising the blend of formal credit and digital finance.

Lavkush Mehra from Bhopal started with a ₹5 lakh loan in 2021 for his pharmaceutical business. Today, his turnover has grown from ₹12 lakh to over ₹50 lakh, and he has become a homeowner — a testament to how timely credit can unlock long-term growth.

Such stories are replicated across India, from rural poultry units and e-rickshaw operators to small food processing and transport ventures.

Strengthening the Ecosystem for Sustainability

Over the past 11 years, PMMY has evolved into a more technology-driven and sustainable framework. Digitisation of transactions, integration with other schemes, and focus on credit quality have improved efficiency. MUDRA Ltd. itself reported strong financial performance, including record profits in recent years, moving towards greater self-sustainability.

The government has continuously refined the scheme — raising the loan limit to ₹20 lakh, introducing Tarun Plus, and emphasising enterprise graduation from micro to small and medium levels. Low Non-Performing Assets (NPAs) in the segment (around 2-3.5% in various reports) demonstrate responsible lending and borrower discipline.

Looking Ahead: From Micro to Resilient Enterprises

As PMMY enters its second decade, the focus is shifting towards higher credit quality, business sustainability, and growth-oriented financing. The goal is clear: help today’s micro-enterprises evolve into tomorrow’s resilient, scalable businesses that contribute more significantly to employment and GDP.

By aligning with initiatives like Digital India, ONDC, and Account Aggregator frameworks, PMMY is preparing micro-entrepreneurs for a more formal, digital, and competitive economy.

Prime Minister Modi and senior leaders have hailed the scheme as a cornerstone of Atmanirbhar Bharat, emphasising how it has boosted self-employment, especially among youth and women.

In conclusion, the Pradhan Mantri MUDRA Yojana has democratised finance for millions. By removing barriers of collateral and complex procedures, it has unleashed the entrepreneurial spirit at the grassroots. As India aims for a $5 trillion economy and greater self-reliance, PMMY continues to play a vital role in building an inclusive, vibrant, and bottom-up growth story — one small loan at a time.