India remains fastest growing economy for 4th consecutive year; pegged economic (GDP) growth at 7.4% in FY26

India continues as the fastest growing economy for the fourth consecutive year despite a fragile geo-political scenario as the economic growth (or the GDP growth) for the current financial year (2025-26) is estimated at 7.4 per cent driven by the double engine of consumption and investment.

“It reaffirms India’s status as the fastest-growing major economy for the fourth consecutive year,” V. Anantha Nageswaran, Chief Economic Advisor, Ministry of Finance said while highlighting the Economic Survey 2025-26 tabled in Parliament today.

The Survey says the real GDP growth for FY27 (next financial year) is projected at 6.8-7.2 per cent, while the potential growth for India is estimated at around 7 per cent.

Asked whether this is good to achieve “Viksit Bharat” by 2047, Nageswaran said “7 percent average growth which is 8 per cent plus in USD terms on a sustainable basis would take India to achieve the target of Viksit Bharat by 2047.

He said that growth momentum in India is fact driven by the positive developments in the domestic economy and India has done well despite the current geopolitical scenario.

The Survey highlights that Agriculture and allied services are estimated to grow by 3.1 per cent in FY26. Agricultural activity in the first half of FY26 was supported by a favourable monsoon. Agricultural GVA grew by 3.6 per cent, higher than the 2.7 per cent growth recorded in the first half of FY25, but remained below the long-term average of 4.5 per cent. Allied activities, particularly livestock and fisheries, have grown at relatively stable rates of around 5-6 per cent. As their share in agricultural GVA has increased, aggregate agricultural growth has increasingly reflected a weighted outcome of volatile crop performance and a relatively stable expansion in allied sectors.

On the inflation front, the CEA said it has softened to an all-time low as the headline CPI (Consumer Price Index) has fallen to 1.7 per cent (up to December, 2025).

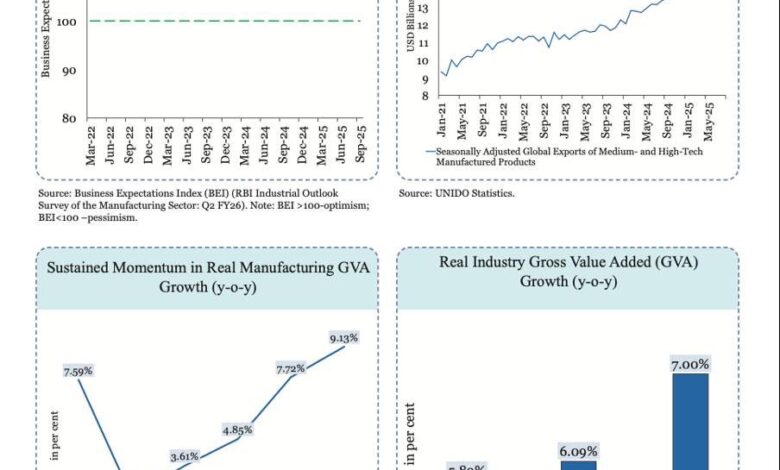

The industrial sector is showing signs of strength, with manufacturing growing by 8.4 per cent in the first half of FY26, surpassing the FY26 estimate of 7.0 per cent. Additionally, the construction industry has remained resilient, underpinned by sustained public capital expenditure and ongoing momentum in infrastructure projects. The manufacturing sector share has remained steady at around 17-18 per cent in real (constant) price terms.

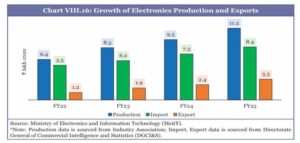

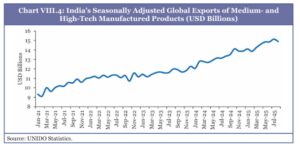

The Economic Survey mentions that against a backdrop of global trade uncertainty, India’s total exports (merchandise and services) reached a record USD 825.3 billion in FY25, with continued momentum in FY26. Despite heightened tariffs imposed by the United States, merchandise exports grew by 2.4 per cent (April–December 2025), while services exports increased by 6.5 per cent. Merchandise imports for April-December 2025 increased by 5.9 per cent. Following the trends in previous years, the rise in merchandise trade deficit has been counterbalanced by an increase in services trade surplus, while the growth in remittances has bolstered this balance. In most years, remittances have surpassed gross FDI inflows, underscoring their importance as a key source of external funding. As a result, the current account deficit remains moderate at 0.8 per cent of GDP in H1 FY26.

India’s external sector is placed comfortably in the short run. Forex reserves cover over 11 months of imports as of 16 January 2026 and approximately 94.0 per cent of the external debt outstanding as of the end of September 2025, offering a comfortable liquidity cushion. The pursuit of a diversified trade strategy, as evidenced by the signing of trade agreements with the UK, Oman, and New Zealand, and the recently concluded free trade agreement with the European Union after three years of negotiations, which will now require ratification by the European Parliament. Moreover, the active negotiations with the US, bodes well for India’s exports.

The Economic Survey is a report card of the government for the previous year and is traditionally placed a day before the Union Budget is presented for the next fiscal on February 1.